Business Blog

It’s a given that companies shouldn’t charge consumers hidden fees. But it raises a particular concern when an online lender makes “No Hidden Fees” claims a centerpiece of its marketing – and then deducts from those loans hundreds or even thousands of dollars in hidden up-front fees.

According to a lawsuit filed by the FTC,  Lending Club, which bills itself as “the world’s largest online marketplace connecting borrowers and investors,” attracts prospective borrowers with direct mail pieces, online ads, and even paid blog posts touting that the loans come with “no hidden fees.” For example, as a Lending Club-created paid-for post on a credit website promises, “Once you’re approved, your money goes straight into your account, with no hidden fees.” But as the complaint alleges, consumers are in for a surprise when they learn that what goes “straight into [their] account” is not the total represented during the online application process as the “Loan Amount.” Instead, what they get is an amount reduced by hundreds or thousands of dollars. That’s because Lending Club takes a hefty portion of the Loan Amount up front as an origination fee.

Lending Club, which bills itself as “the world’s largest online marketplace connecting borrowers and investors,” attracts prospective borrowers with direct mail pieces, online ads, and even paid blog posts touting that the loans come with “no hidden fees.” For example, as a Lending Club-created paid-for post on a credit website promises, “Once you’re approved, your money goes straight into your account, with no hidden fees.” But as the complaint alleges, consumers are in for a surprise when they learn that what goes “straight into [their] account” is not the total represented during the online application process as the “Loan Amount.” Instead, what they get is an amount reduced by hundreds or thousands of dollars. That’s because Lending Club takes a hefty portion of the Loan Amount up front as an origination fee.

You’ll want to read the complaint and see the accompanying visuals to get a feel for what the transaction looks like from the consumer’s perspective. But the FTC alleges that on both computers and smartphones, what little information Lending Club offers about the up-front charge is hidden, often behind obscure hyperlinks or sandwiched between lines of “below the fold” text.

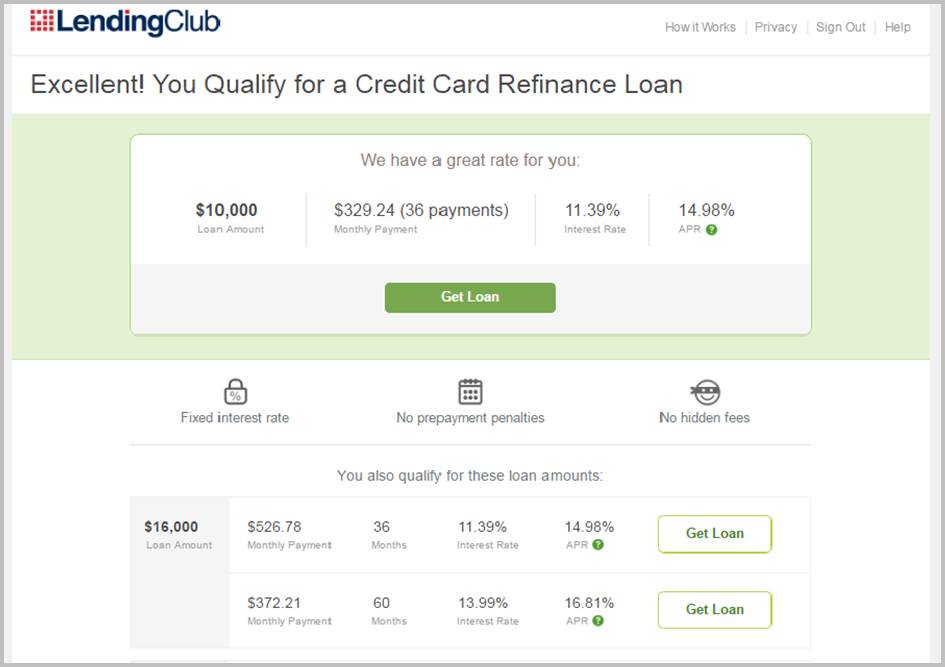

A ccording to the lawsuit, in response to consumer concerns about the undisclosed or inadequately disclosed up-front charge, the company’s own quarterly complaint reviews have proposed “highlighting [the] origination fee.” According to one in-house compliance review, “The origination fee is disclosed on the offer page tooltip” – a small green-and-white hyperlinked question mark – “but is not readily apparent unless an applicant clicks on the tooltip. This omission could be perceived as deceptive as it is likely to mislead the consumer.” One of Lending Club’s largest investors warned the company that the fee “is not clear and conspicuous and could be subject to a UDAAP claim,” referring, of course, to unfair or deceptive acts or practices. In addition, the FTC says the investor’s legal counsel told Lending Club that despite the company’s prominent “no hidden fees” claim, “the documents we reviewed contain a large ($300 to $450) origination fee that only appears once” in “relative obscurity” – a practice the person said could result in law enforcement action.

ccording to the lawsuit, in response to consumer concerns about the undisclosed or inadequately disclosed up-front charge, the company’s own quarterly complaint reviews have proposed “highlighting [the] origination fee.” According to one in-house compliance review, “The origination fee is disclosed on the offer page tooltip” – a small green-and-white hyperlinked question mark – “but is not readily apparent unless an applicant clicks on the tooltip. This omission could be perceived as deceptive as it is likely to mislead the consumer.” One of Lending Club’s largest investors warned the company that the fee “is not clear and conspicuous and could be subject to a UDAAP claim,” referring, of course, to unfair or deceptive acts or practices. In addition, the FTC says the investor’s legal counsel told Lending Club that despite the company’s prominent “no hidden fees” claim, “the documents we reviewed contain a large ($300 to $450) origination fee that only appears once” in “relative obscurity” – a practice the person said could result in law enforcement action.

Did the company respond to those warnings? No, alleges the FTC. According to the complaint, “Rather than improving over time, [Lending Club’s] violations have become more egregious over the years,” with the company increasing the prominence of the “no hidden fees” claim and decreasing the already small, hyperlinked tooltip.

Those allegations relate only to the first of four counts charged in the lawsuit. Regarding Count II of the complaint, Lending Club engages in a two-step review process. The FTC alleges that the company has told consumers things like “Great news! Investors have backed your loan 100%!” when there were still additional hurdles prospective borrowers had to vault, including a stringent second credit review that many people can’t meet. As a result, the FTC says some prospective borrowers who got those congratulatory messages were ultimately rejected, rendering the company’s claims deceptive.

Count III of the complaint alleges that in numerous instances, Lending Club has made unauthorized withdrawals from consumers’ bank accounts – for example, by charging borrowers double payments in a single month, by continuing to make withdrawals from consumers who have paid off their loans, or by taking money from accounts when consumers have told Lending Club they want to pay by check or by a different account. The upshot of the allegedly unfair practice: for some borrowers, unexpected overdraft fees. The complaint also alleges violations of the Gramm-Leach-Bliley Privacy Rule and Regulation P.

The FTC filed the case in federal court in California, but even at this early stage, the complaint is a reminder of how important it is for consumers to have accurate information from lenders – including online marketplace lenders.

April 25, 2018

This amazes me due to timing and other experiences with another lender that was much worse than Lending Club and nothing was done other than the company being put in a file for future complaints and FTC was unable to do anything,,, that was what I was told.

What is unfortunate for me is, I borrowed money from Lending Club as well and you are telling me there is a lawsuit now for their illegal practices. I borrowed $3,000 and $300 was taken before I got the balance of the loan. I understood it to be upfront fee's and I sat up an automatic payment through my bank account. I thought they must be doing a legal transaction and accepted it.

I wish my loan with the previous lender, AVANT, INC, would have been investigated for their illegal procedures because they were destroying my credit rating by giving false information to both the credit bureaus and me. They showed me being late for 30, 60, 120 days which was a lie beyond lies. I missed one payment due to a health emergency and tried to make it up until it got totally out of control and caused me extreme stress. I borrowed the money from Lending Club to pay off the debt. My loan at AVANT was $1300 and I ended up paying almost twice the amount of the loan. They were the most stressful company I have ever dealt with in my life and extremely unprofessional. After researching them, there were many other people that had the same experiences but evidently did not report it to FTC.

I have had no problems with Lending Club, and as I said, I had the understanding it was going to cost me a fee for the loan, and I accepted it. Uneducated with the financial world can be very costly and most consumers are at the mercy of all companies whether legal or not. I have less faith in our BBB and Cpfb and all 3 credit bureau's who are in control of our financial lives because 99% of any problem, the consumer loses.

April 25, 2018

This is what I can't stand when hard working people need extra cash and these crooks scam you. It's not right! They should be in jail. They know their scamming people! Shame on Lending Club!!

April 26, 2018

Add me. I have taken out two loans with them. One is now paid off and the other due to be paid off in a few months.

May 05, 2018

This is an eye opener for me as I took a loan with Lending Club about 3-5 years ago to save on interest on those credit card debts. I have since paid off that loan. And now, I just took out another loan this year to pay off two credit cards. It will be interesting to see what the outcome on this case will be, and whether borrowers will be refunded those hidden fees.

May 23, 2018

I have a loan through lending club that will be paid off in a few months and I've used them for previous loan. I also expected(on my first loan) that there would be a fee taken out of the loan amount before I received the remaining amount. I accounted for that when determining how much to borrow. As an adult, I don't expect to get a loan for free. The loan documents, have all the information disclosed. Personally, I didn't rely on the web page for the final details of the loan obligation I was entering into.

June 18, 2018

I just received a loan from them and YES they did take out fee whithout my knowledge. I took the loan anyway since I had NO choice. Can you HELP?

August 08, 2018

I am so glad that real lenders still exists, My name is Maria Hernandez From Texas ,

Just Yesterday I got my bad credit loan of $15000 from Mr Lavington who is from North Carolina USA,

I saw his advert Online and applied directly by contacting his email : lavingtonfinance@gmail.com

and I also called his phone number +18288270635 for confirmation , He replied me and gave me the loan at interest of 2% ,

Surprisingly within 24 hours my bank account was credited with the loan.

This Loan Process was so Sweet,Fast,StraightForward,Real,Amazing, and Unique, I did my part and Mr Lavington did not fail me ,

So I reccommend all serious borrowers to get their best loan from lavingtonfinance@gmail.com or call +18288270635 .

Do not pass this post bye if you are a serious borrower because the Lavington Finance Service is Amazing,

Best Thanks You All.