Business Blog

Top picks, star ratings, in-depth reviews. Many consumers don’t buy anything without consulting third-party review sites or checking out the opinions of other customers. But how often are those ratings the product of buying and selling between the “independent” site and companies willing to pay for better play? And are those reviews really from satisfied customers or are they from employees acting on instructions to stuff the ballot box with five-star ratings? Those are the allegations in a lawsuit against LendEDU, a site the FTC says falsely claimed to offer “objective” evaluations of financial products. Does the proposed settlement in this case suggest it’s time to review your own review practices?

Many consumers comparison-shopping for student loans, personal loans, and credit cards visited LendEDU based on its promise of “honest,” “accurate,” and “unbiased” ratings and reviews. For example, LendEDU’s student loan refinancing page offered a rate table, rankings, star ratings, and reviews of what it claimed were the best or top companies. LendEDU and its corporate officers hammered home the message that due to their “strict editorial integrity,” those ratings “are completely objective and not influenced by compensation in any way.” False, says the FTC.

According to the complaint, LendEDU boosted companies’ numerical ranking and position on rate tables based on payments to LendEDU. For example, in an email to a student loan refinancing company whose rating had fallen from #1 to #3, LendEDU’s CEO said it could retake the top spot by paying LendEDU $9.50 per click. LendEDU’s Vice President of Product later contacted the same company, suggesting it increase the payment to $16.50 per click: “We want to keep [your company] positioned as the #1 lender on our site, but we need to justify the move from a business perspective.” The company ultimately agreed to pay $15 per click, and LendEDU kept the company in the top spot. The complaint alleges that LendEDU offered another student loan refinancing company the #3 position for a payment of $16 per click. The contract expressly provided for a ranking “[n]o lower than position 3.”

The complaint recounts other examples of how the FTC says LendEDU finagled the ratings for pay. What were consumers told about these arrangements? Up until mid-2016, nothing. Then LendEDU added a fine-print sentence at the bottom of its website that the “site may be compensated through third party advertisers.” Around March 2019 – after LendEDU learned of the FTC’s investigation – it listed elsewhere on its site the companies that “may provide compensation to LendEDU.” But the FTC says those “disclosures” were placed where consumers were unlikely to see them.

That’s not the only way LendEDU allegedly deceived consumers. On its own site and on third-party review platforms, supposedly satisfied customers raved about their experience with LendEDU. For example, on Trustpilot, 123 of 126 reviews gave LendEDU the highest five-star rating. Here’s what three purported consumers had to say:

- Kenny: “LendEDU showed me the light at the end of the tunnel. I was drowning in student loan debt then they showed up with a lifeboat and a warm blanket. The website was easy to navigate and with the help of their customer service team, I saved a lot of money refinancing. I can’t thank them enough and would recommend to anyone!

- Scott: “Extremely user friendly and easy to use. . . . It was a pleasant surprise to be able to find personal finance education. As a student, high schools don’t really provide any basic financial course and credit cards are so easy to obtain. It was refreshing to be able to research and understand more through LendEDU.

- Trace: “I wasn’t sure where to go, and stumbled onto an[] article LendEDU published. It was full of good tips that helped. I ended up going to their site and there was quite a bit of helpful stuff there too. They seem to be on top of it!”

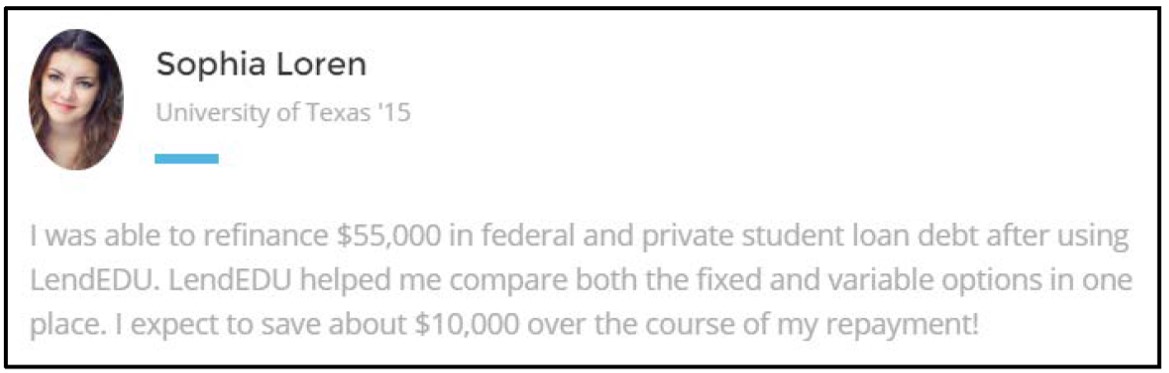

But according to the FTC, “Kenny” was a LendEDU employee, “Scott” administered the company’s 401(k) plan, and “Trace” was a friend of someone who worked at LendEDU. In addition, LendEDU featured on its own site testimonials from supposedly satisfied customers. For example, one consumer who offered a glowing recommendation was identified as “Sophia Loren.” No, not that Sophia Loren. But according to the FTC, it wasn’t any other Sophia Loren either since LendEDU fabricated the endorsement.

But according to the FTC, “Kenny” was a LendEDU employee, “Scott” administered the company’s 401(k) plan, and “Trace” was a friend of someone who worked at LendEDU. In addition, LendEDU featured on its own site testimonials from supposedly satisfied customers. For example, one consumer who offered a glowing recommendation was identified as “Sophia Loren.” No, not that Sophia Loren. But according to the FTC, it wasn’t any other Sophia Loren either since LendEDU fabricated the endorsement.

The complaint charges that LendEDU and three corporate officers falsely represented that ratings and rankings weren’t influenced by compensation, failed to disclose adequately that they were paid for ratings and rankings, and falsely claimed that fake testimonials were the opinions of impartial consumers. The proposed settlement puts court-enforceable provisions in place to address LendEDU’s deceptive practices, requires clear disclosures in the future, and includes a financial remedy of $350,000. Once the proposed settlement appears in the Federal Register, the FTC will accept public comments for 30 days.

What can other companies take from the case?

Honor your claims about objectivity. Lots of sites represent themselves as honest brokers of accurate information. But if you claim that compensation doesn’t factor into your content, that has to be a truthful statement. Also, if you receive compensation from companies you rate or rank, would that financial connection be material to consumers in deciding whether to do business with those companies? If so, clearly disclose the connection.

Avoid “behest-imonials.” This isn’t the first time the FTC has challenged deceptive reviews, endorsements, or testimonials. There are at least three ways that posting customer reviews can go off the rails: 1) if the reviews don’t reflect the actual experience of the reviewers; 2) if there is an undisclosed material connection between the reviewer and advertiser – for example, if the reviewer is an employee, friend, or family member; and 3) if the advertiser fabricates reviews from whole cloth. Visit the FTC’s Endorsements, Influencers, and Reviews page for compliance resources.

February 03, 2020

LENDEDU IS NOT THE ONLY COMPANY THAT DOES THIS MANY CEOS PAY THEIR EMPLOYEES TO COMMENT ON PRODUCTS PLACE OF BUSINESS AND EMPLOYEES ARE ACTUALLY WILLING. BUT THERE ARE ALOT IF DECEPTION IN THE RETAIL AND FINANCIAL SECTORS.