Business Blog

For consumers already underwater financially and desperate for just $50, cash advance company FloatMe’s services turned out to be more sink than swim. According to the FTC, the subscription-based business violated the FTC Act, the Restore Online Shoppers’ Confidence Act (ROSCA), and the Equal Credit Opportunity Act (ECOA) by using deceptive and unfair tactics against its customers, including people on Social Security and veterans receiving military pensions. In addition to $3 million in consumer redress and provisions that will change how FloatMe does business in the future, the settlement includes a provision specifically prohibiting deceptive claims about the use of artificial intelligence, algorithms, or machine learning.

Image

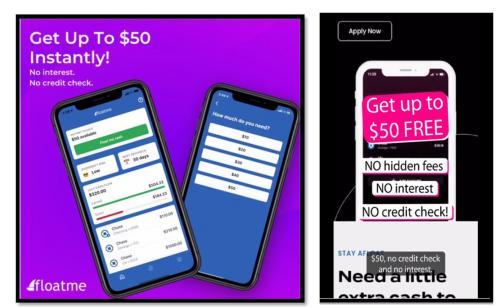

FloatMe operates a mobile app that claims to offer consumers who pay a $1.99 monthly subscription fee small short-term cash advances – called Floats – that are automatically debited from consumers’ bank accounts on their next payday. How small? FloatMe advertises that consumers can “get up to $50 instantly,” suggesting that the company targeted people struggling to make ends meet. But consumers who tried to get $50 rarely got even that much from FloatMe. What they did get was a raft of undisclosed fees and hassles when they tried to cancel.

On its website and in social media, FloatMe claimed that consumers could get cash “instantly,” “now,” and “in minutes” with “no hidden fees” and “no interest.” According to one FloatMe ad, “All you have to do is download the FloatMe app. It’s free. It’s easy to get to. Sign up for the membership and get $50 free money” – promises the company reinforced when consumers downloaded the app from the Apple App Store or the Google Play Store. FloatMe also said consumers could “Cancel anytime for any reason by contacting support.”

That’s what the company claimed, but according to the FTC, FloatMe limited the amount consumers could get at signup to – at most – $20. What’s more, in the most recent quarter, less than 5% of consumers received a Float of more than $20, even after paying subscription fees for years. The FTC also says that during that same period, only one half of one percent of consumers received a $50 Float.

When consumers sought an increased cash advance, FloatMe sometimes claimed those limits were “automatically” increased by an “algorithm” as the company “gets to know [consumers] better.” In fact, there was no such algorithm. And despite FloatMe’s repeated promises of “instant” cash with “no hidden fees,” consumers couldn’t get money “instantly” unless they paid an additional $4 charge. Otherwise they had to wait three days – a catch the FTC says FloatMe didn’t clearly disclose up front.

Other customers paid their monthly fees to FloatMe only to learn that the company considered them ineligible to receive any money at all. To get a Float, FloatMe required consumers to meet certain income thresholds, but didn’t count income derived from gig work, tips, pensions, military benefits, or public assistance programs, including Social Security – conditions the FTC alleges FloatMe didn’t clearly disclose to consumers. As the complaint puts it, “At least tens of thousands of paying consumers have been prevented from even requesting a cash advance because of these undisclosed eligibility requirements. These consumers are still charged subscription fees, even though FloatMe deems them categorically ineligible to receive Floats.”

For consumers who wanted to cancel their subscriptions, the headaches were just beginning as they had to navigate multiple ineffective cancellation options before the company would stop debiting their bank accounts. In other instances, the FTC says FloatMe simply ignored cancellation requests and continued to help themselves to consumers’ bank accounts. Messages FloatMe received from its customers expressed frustration with the company’s practices – for example:

- “I downloaded the app for this company. I was not eligible for loans so I canceled my membership . . . . They have continuously charged me monthly, I have canceled my subscription three times on the app, emailed them three times, received responses confirming cancellation, and they are still charging me monthly.”

- “I closed my account several months ago but I woke up yesterday to my account going negative because they billed me for a subscription. . . and it’s nearly impossible to get a hold of anybody in customer service. Scam company.”

- “I was told the solution to cancelling the membership was a link I could click to fill out a cancellation form, once I clicked the link the page was expired and I have absolutely no way to get them to stop charging me money. I downloaded this app because I was struggling and needed help and all it has done is make things worse and never offer remedy.”

You’ll want to read the complaint for evidence from the company’s own internal documents, but the FTC summarizes it this way: “FloatMe explicitly designed its cancellation processes to thwart consumers’ ability to cancel so that the company could reap more subscription fees.”

The lawsuit alleges FloatMe and corporate officers Joshua Sanchez and Ryan Cleary violated the FTC Act by making deceptive claims about cash advances, falsely claiming consumers could get advances immediately without having to pay extra, and unfairly charging consumers without their consent. The FTC says the defendants also violated ROSCA by failing to make required disclosures, failing to get consumers’ express informed consent before charging them, and failing to provide a simple mechanism for stopping recurring charges. In addition, the complaint alleges the defendants violated the Equal Credit Opportunity Act by disqualifying people whose income came from public assistance programs. In addition to the $3 million financial remedy, the order requires the company to implement a fair lending program similar in form to other FTC actions alleging ECOA violations.

The action against FloatMe includes compliance lessons for businesses offering similar services, but the advice extends beyond that industry.

Online cash advance companies, the FTC is watching how you treat your customers. In bringing its second case against an online cash advance company in just two months, the FTC’s message to industry members should be clear: Established consumer protection laws, including fair lending regulations, apply to your practices and the FTC stands ready to challenge illegal conduct, especially when it injures consumers already struggling to keep their heads above water.

Explain key terms up front. Decades of FTC enforcement establish that advertisers should explain the nature of the transaction up front. Withholding keys terms until after a person signs up – or burying material information where they’re not likely to see it and understand it – violates well-settled consumer protection principles.

For subscription businesses, building “friction” into the cancellation process is a major mistake. Making it easy to enroll and hard to cancel is bad business for companies that use a subscription model – and using dark patterns to retain subscribers against their will make matters even words. Evidence of deficient procedures may be as close as your inbox. Savvy marketers listen to what their consumers are telling them and modify their practices accordingly.

Don’t make false AI-related claims. Some companies pepper their marketing communications with jargon du jour – like “artificial intelligence” or “algorithms” – perhaps just to sound tech-y or sophisticated, But using those words in a false or deceptive way violates established consumer protection standards. Like any other objective claim, a statement about your company’s use of AI or algorithms requires appropriate substantiation.

It is your choice whether to submit a comment. If you do, you must create a user name, or we will not post your comment. The Federal Trade Commission Act authorizes this information collection for purposes of managing online comments. Comments and user names are part of the Federal Trade Commission’s (FTC) public records system, and user names also are part of the FTC’s computer user records system. We may routinely use these records as described in the FTC’s Privacy Act system notices. For more information on how the FTC handles information that we collect, please read our privacy policy.

The purpose of this blog and its comments section is to inform readers about Federal Trade Commission activity, and share information to help them avoid, report, and recover from fraud, scams, and bad business practices. Your thoughts, ideas, and concerns are welcome, and we encourage comments. But keep in mind, this is a moderated blog. We review all comments before they are posted, and we won’t post comments that don’t comply with our commenting policy. We expect commenters to treat each other and the blog writers with respect.

We don't edit comments to remove objectionable content, so please ensure that your comment contains none of the above. The comments posted on this blog become part of the public domain. To protect your privacy and the privacy of other people, please do not include personal information. Opinions in comments that appear in this blog belong to the individuals who expressed them. They do not belong to or represent views of the Federal Trade Commission.