For Release

FTC, Multiple Law Enforcement Partners Announce Crackdown on Deception, Fraud in Auto Sales, Financing and Leasing

Commission Announces Six New Auto Cases in Operation Ruse Control

The .gov means it’s official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information, make sure you’re on a federal government site.

The site is secure.

The https:// ensures that you are connecting to the official website and that any information you provide is encrypted and transmitted securely.

The Federal Trade Commission and 32 law enforcement partners today announced the results of Operation Ruse Control, a nationwide and cross-border crackdown to protect consumers when purchasing or leasing a car, encompassing 252 enforcement actions. The six new FTC cases include more than $2.6 million in monetary judgments.

There were 187 enforcement actions in the United States since the agency’s last sweep, and 65 actions in Ontario and British Columbia, Canada. Enforcement efforts by the FTC, United States Attorney’s Office in the Northern District of Alabama and other partners at the federal, state and local level in the U.S. and Canada include both civil and criminal charges of deceptive advertising, automotive loan application fraud, odometer fraud, deceptive add-on fees, and deceptive marketing of car title loans.

(click to enlarge)

“For most people, buying a car is one of the largest purchases they’ll make,” said Jessica Rich, Director of the FTC’s Bureau of Consumer Protection. “Car ads must be truthful, loan terms must be clear, and dealer practices must be honest. That’s why our partners are working together to crack down on deceptive marketing about car sales, leasing and financing.”

"Growing fraud and other deceptive practices in auto sales and financing are important issues affecting consumers when they are buying a vehicle," said Joyce White Vance, United States Attorney for the Northern District of Alabama. "My office has worked closely with the FTC on this issue, and has prosecuted criminal cases at a Birmingham dealership. The Mortgage, Loan Fraud and Discrimination Working Group of the Attorney General’s Financial Fraud Enforcement Task Force also is working with other law enforcement agencies to determine what we can do now to prevent fraud during the auto lending process."

For the first time since receiving expanded authority over auto dealers under the Dodd-Frank Act, the FTC has taken two auto enforcement actions involving add-ons, which is the practice of a dealer or other third party adding to the vehicle sales, lease, or finance agreement charges for other products or services. A few examples include extended warranties, payment programs, guaranteed automobile protection (commonly called GAP or GAP insurance), credit life insurance, road service, theft protection, and undercoating.

National Payment Network, Inc. (NPN): The FTC charged that NPN, headquartered in San Mateo, Calif., allegedly violated the FTC Act by deceptively pitching consumers an auto payment program – both online and through a network of authorized auto dealers -- that it claimed would save consumers money. NPN failed to disclose that the significant fees it charged for the service often cancelled out any actual savings. The fees to enroll in NPN’s program averaged $775 on a standard five-year auto loan.

Matt Blatt Inc. and Glassboro Imports, LLC (Matt Blatt dealerships): In a related case, the FTC alleged that Matt Blatt dealerships, with multiple locations in New Jersey, violated the FTC Act by failing to disclose or adequately disclose the fees associated with NPN’s add-on service and that many consumers would not save money overall due to the program’s significant fees. Matt Blatt dealerships received a commission for each of the more than 1,000 consumers they enrolled.

NPN and Matt Blatt dealerships have agreed to settle the FTC charges, and under proposed consent orders are prohibited from misrepresenting that a payment program will save consumers money, unless the amount of savings is greater than the total amount of fees and costs charged in connection with the program. They also are prohibited from misrepresenting that the payment programs or their associated fees will improve, repair or otherwise affect a consumer’s credit record.

NPN will refund more than $1.5 million to consumers, and waive another $949,000 in fees to current customers during the fee waiver period. Matt Blatt dealerships also will pay $184,000 to the FTC as part of the settlement.

The Commission votes to issue the two administrative complaints and to accept the proposed consent orders were 5-0. The agreements are subject to public comment for 30 days, beginning today and continuing through April 27, 2015, after which the Commission will decide whether to make the proposed consent orders final. Submit a comment electronically:

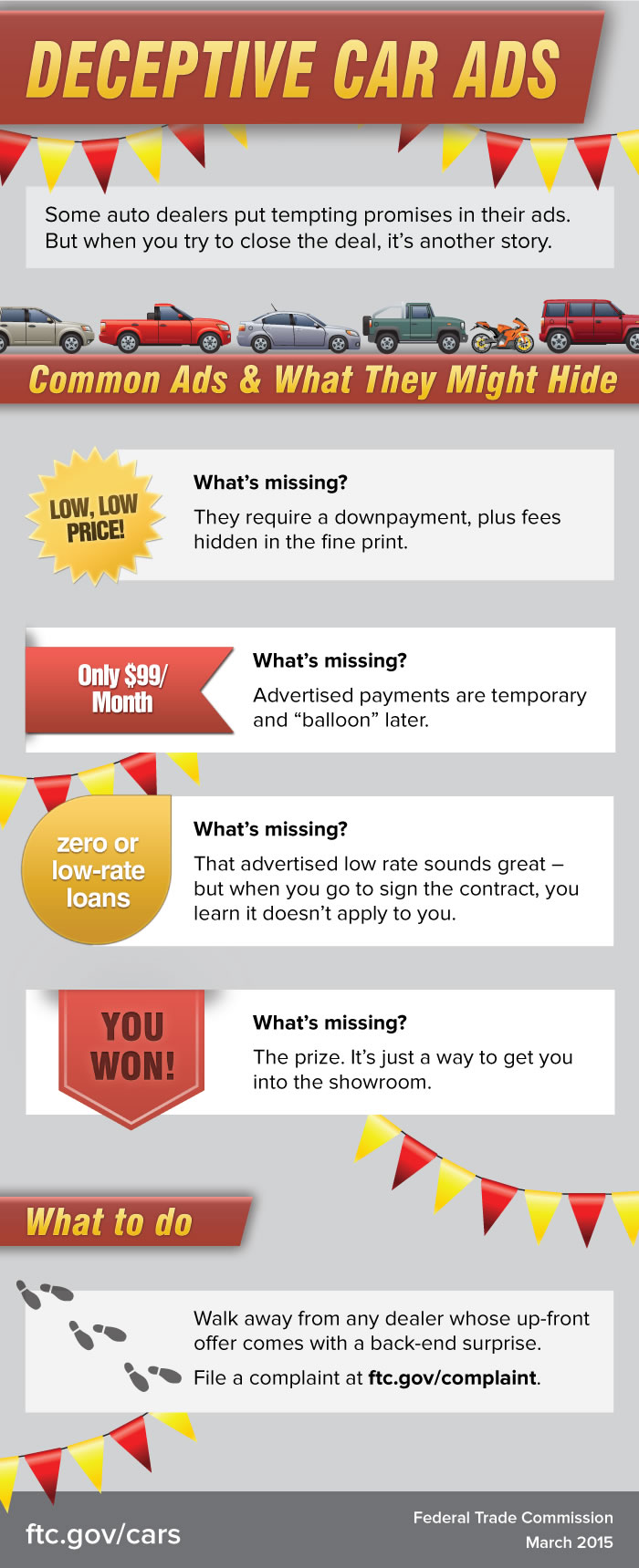

Three auto dealers, Cory Fairbanks Mazda of Longwood, Fla., Jim Burke Nissan of Birmingham, Ala., and Ross Nissan of El Monte, Calif., have agreed to settle charges that they ran deceptive ads that violated the FTC Act, and also violated the Truth in Lending Act (TILA) and/or Consumer Leasing Act (CLA). According to the FTC complaints, ads touted sales, lease or financing options that seemed attractive but were cancelled out by fine-print disclaimers. In other instances, the disclaimers did not disclose relevant terms, such as required down payments.

All of the financing offers, lease payments, and $0 down references in this ad are completely undermined by the fine print, which requires $3,000 down for all deals.

Click to view the fine print section.

The proposed settlements in these actions prohibit the defendants from misrepresenting the purchase cost or any other material fact about the price, sale, financing or leasing of a vehicle. Jim Burke Nissan and Cory Fairbanks Mazda are also prohibited from representing that a discount, rebate, bonus, incentive or price is available unless it is available to all consumers or all qualifications and restrictions are clearly and conspicuously disclosed. The proposed orders also address the TILA and CLA violations by requiring the dealerships to clearly and conspicuously disclose terms required by these rules.

The Commission votes to issue the three administrative complaints and accept the proposed consent orders were 5-0. The agreements will be subject to public comment for 30 days, beginning today and continuing through April 27, 2015, after which the Commission will decide whether to make the proposed consent orders final. Submit a comment electronically:

The FTC thanks the Consumer Protection Division of the Florida Office of the Attorney General in the Cory Fairbanks Mazda matter and the Los Angeles County Department of Consumer and Business Affairs in the Ross Nissan matter for their collaborative efforts and support. The FTC also would like to thank the South Carolina Department of Consumer Affairs for their contributions to this initiative.

Auto Loan Modification Case

At the FTC’s request, the U.S. District Court for the Southern District of Florida temporarily halted the practices of Regency Financial Services of Lake Worth, Fla., and its CEO Ivan Levy, who allegedly charged consumers upfront fees to negotiate an auto loan modification on their behalf, but then often provided nothing in return. The court also froze defendants’ assets, and last month entered a Stipulated Preliminary Injunction Order. The FTC’s lawsuit filed on Jan. 26, 2015 is ongoing, and the Commission is seeking a permanent injunction to stop defendants’ deceptive practices and to return ill-gotten gains to consumers.

According to the FTC’s complaint, defendants violated the FTC Act and Telemarketing Sales Rule by misrepresenting that they would obtain auto loan modifications for consumers and provide full refunds if they failed to do so.

The Commission vote authorizing staff to file the complaint was 5-0.

The FTC thanks the Florida Office of Financial Regulation for their support in this case.

This operation follows the FTC’s sweep against 10 auto dealers announced in January 2014, and is part of the agency’s ongoing effort to protect consumers purchasing and financing a new vehicle.

Consumers in the market for a new or used vehicle should read the FTC’s new blog post, Add-On Auto Finance Plan Gets a “D” for Deception, along with Are Car Ads Taking You for a Ride? and Buying and Owning a Car. Businesses can check out new guidance in the FTC’s blog post: Operation Ruse Control: 6 Tips If Cars Are Up Your Alley.

NOTE: The Commission files a complaint when it has “reason to believe” that the law has been or is being violated and it appears to the Commission that a proceeding is in the public interest. The issuance of the administrative complaint marks the beginning of a proceeding in which the allegations will be tried in a formal hearing before an administrative law judge.

The Federal Trade Commission works for consumers to prevent fraudulent, deceptive, and unfair business practices and to provide information to help spot, stop, and avoid them. To file a complaint in English or Spanish, visit the FTC’s online Complaint Assistant or call 1-877-FTC-HELP (1-877-382-4357). The FTC enters complaints into Consumer Sentinel, a secure, online database available to more than 2,000 civil and criminal law enforcement agencies in the U.S. and abroad. The FTC’s website provides free information on a variety of consumer topics. Like the FTC on Facebook, follow us on Twitter, and subscribe to press releases for the latest FTC news and resources.

MEDIA CONTACT:

Cheryl Warner

Office of Public Affairs

202-326-2480

STAFF CONTACTS:

Cindy Liebes (Regency Financial, Cory Fairbanks, and Jim Burke)

Southeastern Regional Office

404-656-1359

Dan Dwyer (NPN and Matt Blatt)

Bureau of Consumer Protection

202-326-2957

John Jacobs (Ross Nissan)

FTC’s Western Regional Office – Los Angeles

310-824-4360

Peggy Sanford

U.S. Attorney’s Office

Northern District of Alabama

205-244-2020